The DSO Decade-Long Creep

In 2015, the global corporate environment was defined by near-zero interest rates and abundant cheap debt. This created a regime of "apathy" toward working capital; with the cost of borrowing so low, CFOs felt little pressure to aggressively collect receivables. By 2025, however, the landscape shifted violently. High interest rates and inflation forced a return to the mantra "Cash is King," yet despite this, Days Sales Outstanding (DSO), the primary metric of cash collection efficiency, has structurally deteriorated across nearly every major industry.

The average global DSO has climbed significantly, trapping billions of dollars in supply chains. Instead of generating cash through operations, suppliers have been forced into the role of "Hidden Bankers," extending trade credit to support customers who are themselves facing liquidity crunches.

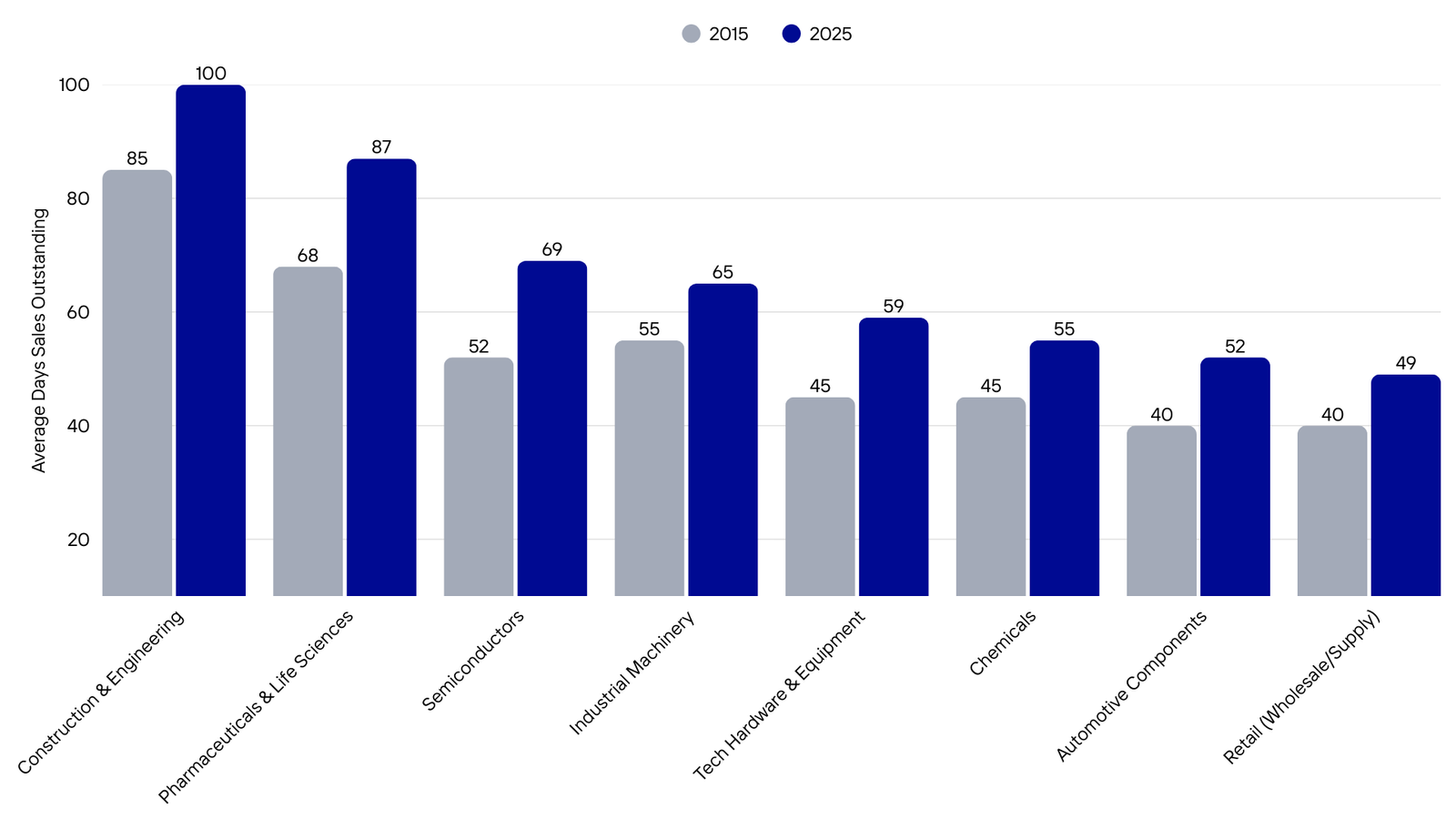

Industry Trends: 2015 vs. 2025

The data illustrates the absolute increase in the average number of days it takes for companies to convert a sale into actual cash across key sectors.

Why DSO Has Climbed: Four Primary Forces

The decade-long rise in DSO is a derivative of macroeconomic shifts and changing balance-of-power dynamics. Four core forces have driven this across-the-board increase:

1. Extended Customer Payment Terms

Many companies have granted more lenient credit terms, often under pressure from large, consolidated customers. Over the past decade, standard net-30 terms have stretched to 60 or even 90 days in certain sectors. Buyers now wield greater bargaining power to demand longer payment windows, effectively using their suppliers as interest-free financing.

2. Economic Shocks and Cash Preservation

Major events, specifically the 2020 pandemic, forced buyers to deliberately delay payments to shore up their own cash reserves. This behavior became "sticky"; even after the initial crisis subsided, persistent uncertainty regarding inflation and geopolitical fragmentation has kept customers cautious and slower to pay.

3. The Impact of Low Interest Rates (2010s)

During the majority of the 2010s, capital was so cheap that working capital discipline slipped. Finance teams were less focused on tightening DSO when debt financing was virtually "free". This complacency allowed DSO to drift upward, and only now, with interest rates tripling or quadrupling the cost of carry, are companies urgently re-focusing on collection speed.

4. Structural Friction and Complex Billing

In industries like Healthcare and Pharmaceuticals, increased regulatory hurdles and insurance claim complexities have prolonged the receivables cycle. Similarly, the shift toward "Hardware-as-a-Service" and subscription-based models in Tech has created monthly billing cycles that are inherently slower than traditional upfront sales.

The Path Forward: Closing the Gap

Reining in DSO is now a top priority for financial leadership. The math is simple: for every $100M in annual revenue, reducing average DSO by just 10 days can generate a $3M lift in cash and over $300,000 in annual interest savings.

To close the gap, companies are moving beyond manual outreach and adopting digitized, AI-driven Accounts Receivable (AR) practices:

- Real-Time Visibility: Centralizing data to flag high-risk accounts early and prioritize collection efforts based on cash impact.

- Dynamic Credit Policies: Shifting from "standard terms" to dynamic terms based on a customer's real-time credit risk.

- Automated Workflows: Using tools to enforce prompt, systematic follow-ups, reducing the "slip-throughs" that prolong the payment cycle.

Ultimately, the goal for 2026 is for finance teams to reclaim control of their cash flow, ensuring that their organization's balance sheet is used for growth rather than acting as an involuntary bank for their customers.

Sources

- • Hackett Group Working Capital Surveys (2015, 2025)

- • Allianz Trade Global DSO Report 2025

- • J.P. Morgan Working Capital Index 2024

Ready to Scale Your AR Team?

See how Domeo can transform your accounts receivable operations in days.

Request a Demo